|

I would like to personally thank ALL of our Service Members, Veterans and

eligible surviving spouses for your sacrifice to our country! I'm

always grateful for the opportunity to help military families buy & sell

homes in the Denver Metropolitan area. I work with retired military

buyers and sellers & assist military families who are relocating or transitioning from active-service to various civilian

employment with defense contractors such as Lockheed Martin, General

Dynamics, Northrop Grumman, Boeing & Raytheon. I consider it an

honor and a privilege to provide expert, professional real estate services

to military families and I look forward to help you buy or sell a home. Anthony Rael, your VA Military-friendly Realtor with RE/MAX

Alliance - 303-520-3179

As an experienced VA/Military-friendly Denver

Realtor with RE/MAX, I am fortunate to recommend local VA Mortgage

Lenders who understand the VA mortgage loan process and will work

hard to secure the best VA loan possible. Since VA guarantees a

portion of the loan, this enables the mortgage lender to provide you with

more favorable terms (saving you thousands of dollars!).

Get Pre-Qualified for a

VA Home Loan

Today!

Preferred VA Mortgage Lenders for

Anthony Rael, RE/MAX Alliance - Denver Realtor

* Home

Mortgage Advisors - Stephany

Overmyer - 419.376.0318

* Peak

10 Mortgage LLC - Tenby

J. Dahman - 303.478.9126

Buyer 24-Month Investment Protection

Program

Buyer 24-Month Investment Protection

Program

What is a VA

Guaranteed Home Loan?

VA guaranteed loans are made by private lenders, such as banks,

savings & loans, or mortgage companies to eligible veterans for the

purchase of a home which must be for their own personal occupancy. The

guaranty means the lender is protected against loss if you fail to repay

the loan. The guaranty replaces the protection the lender normally

receives by requiring a down payment allowing you to obtain favorable

financing terms.

VA Loan vs.

Traditional Mortgages

Military homebuyers have access

to one of the most unique and powerful loan programs ever

created. See how the VA Loan compares to a traditional home

mortgage: |

|

VA Loans |

Conventional

Loans |

0% Down

(for qualified

borrowers)

VA Loans are among the last 0% down home loans

available on the market today. |

Up to 20% Down

Conventional loans generally

require down payments that can reach up to 20% to secure a

home loan, pushing them out of reach for many homebuyers. |

|

No PMI

Since VA Loans are government

backed, banks do not require you to buy Private Mortgage

Insurance (PMI). |

PMI Required

Private Mortgage Insurance is a

requirement for borrowers who finance more than 80% of their

home's value, tacking on additional monthly expenses. |

|

Competitive Interest Rates

The VA guaranty gives lenders a greater degree

of safety and flexibility, which typically means a more competitive rate

than non-VA loans. |

Increased Risk for Lenders

Without government backing, banks are taking on

more risk which, in turn, can result in a less-competitive interest rate on

your home loan. |

|

Easier to Qualify

Because the loan is backed by

the government, banks assume less risk and have less

stringent qualification standards for VA Loans, making them

easier to obtain. |

Standard Qualification

Procedures

Conventional options hold stricter

qualification procedures that can put homeownership out of reach for some

homebuyers. |

VA Home Loan Benefits

Purchase Loans help you purchase a home at a

competitive interest rate often without requiring a down payment or

private mortgage insurance. Cash Out Refinance loans allow you to take

cash out of your home equity to take care of concerns like paying off

debt, funding school, or making home improvements.

VA Home Loan Limits

As of January 2025, if you have full entitlement, there is no VA

mortgage loan limit. However, each county throughout the country has loan

limits based on where you want to live. These are referred to as "county

limits" and are based upon average & median home prices in a given area.

These limits are very generous and change annually, so please reach out

to Anthony for specific county info.

You have full entitlement if you meet either of

the requirements listed below. At least one of these must be true. You

have:

• Never used your home loan benefit, or

• Paid a previous VA loan in full and sold the property (in this

case, you’d have your full entitlement restored), or

• Used your home loan benefit, but had a foreclosure or compromise

claim (also called a short sale) and repaid us in full

You can use your remaining entitlement - either

on its own or together with a down payment - to take out another VA home

loan.

You may have remaining entitlement if any of these are true:

• You have an active VA loan you’re still paying back, or

• You paid a previous VA loan in full and still own the home, or

• You refinanced your VA loan into a non-VA loan and still own the home,

or

• You had a compromise claim (or short sale) on a previous VA loan and

didn’t repay us in full, or

• You had a deed in lieu of foreclosure on a previous VA loan (this

means you transferred your home’s title to the bank that holds your

mortgage to avoid foreclosure), or

• You had a foreclosure on a previous VA loan and didn’t repay the VA in

full

Is the “limit” the amount I can borrow or the

amount VA guarantees?

The VA-backed home loan limit refers to the amount he VA will guarantee

(the maximum amount the VA will pay to your lender if you default on

your loan). The VA does not limit how much you can borrow to finance a

home.

Eligibility

Requirements

The length of your service or service commitment and/or duty status may

determine your eligibility for specific home loan benefits.

Purchase Loans and Cash-Out

Refinance: VA-guaranteed loans are available for homes for your own

personal occupancy. To be eligible, you must have a good credit score,

sufficient income, a valid Certificate of Eligibility (COE), and meet

certain service requirements.

Why does my COE say,

“This Veteran’s basic entitlement is $0”?

This line on your COE is information for your lender. It shows that

you’ve used your home loan benefit before and don’t have remaining

entitlement. If the basic entitlement listed on your COE is more than

$0, you may have remaining entitlement and can use your benefit again.

On your COE, in the table called Prior Loans charged to entitlement, the

VA will list the amount of your entitlement you’ve already used under

the Entitlement Charged column. Your entitlement can be restored when

you sell your property and pay your VA-backed loan in full, or repay in

full any claim the VA has already paid.

VA Funding Fee

The VA Funding Fee is paid directly to the Department of Veteran's

Affairs and is the reason they can guarantee this no-money-down loan

program. This fee is paid so that VA eligible borrowers can enjoy loan

benefits such as $0 down financing and no PMI payments.

VA Funding Fee Chart

The Funding Fee is calculated by looking

at 5 different factors: Loan amount, loan type (Purchase or Refinance),

type of service, down payment (if any) and prior VA loan use. Take a

look at the charts below to see how the VA

Funding Fee varies based on these

factors:

| |

If your down payment

is… |

Your VA funding fee will be… |

|

First use |

Less than 5% |

2.3% |

|

|

5% or more |

1.65% |

|

|

10% or more |

1.4% |

|

After first use |

Less than 5% |

3.6% |

|

|

5% or more |

1.65% |

|

|

10% or more |

1.4% |

The VA funding fee is a one-time

payment that the Veteran, service member, or survivor pays on a

VA-backed or VA direct home loan. This fee helps to lower the cost

of the loan for U.S. taxpayers since the VA home loan program

doesn’t require down payments or monthly mortgage insurance.

Note: The

VA funding fee rates for these loans don’t change based

on your down payment amount or whether you’ve used the VA

home loan program in the past.

Who pays for which closing costs?

The seller must pay the following

closing costs on your behalf (aka “seller’s concessions”):

-

Commission for real estate

professionals

-

Brokerage fee

-

Buyer broker fee

-

Termite report (very uncommon in

Colorado due to our dry climate)

Additionally, all of the remaining closing costs can be

negotiated as part of the purchase contract:

-

VA funding fee

-

Loan processing fee

-

Loan discount points or funds for

temporary “buydowns”

-

Credit report and payment of any

credit balances or judgments

-

VA appraisal fee

-

Hazard insurance and real estate

taxes

-

State and local taxes

-

Title insurance (paid by seller

99% of the time)

-

Recording fee

Note: Per VA rules, the seller cannot pay more than 4% of the

total home loan in seller’s concessions. But this rule only

covers some closing costs, including the VA funding fee. The

rule doesn’t cover loan discount points.

When is the VA funding fee paid?

-

It can be included or "rolled

back" in to your total loan and it just becomes part of your

monthly mortgage payment, or

-

You also have the option of

paying the full fee out-of-pocket at closing

Will I have to pay the VA funding fee?

If you’re using a VA home loan to buy, build, improve, or

repair a home or to refinance a mortgage, you’ll need to pay the VA

funding fee unless you meet certain requirements. You will not have

to pay a VA funding fee if any of the below descriptions are true:

-

Receiving VA compensation for a

service-connected disability, or

-

Eligible to receive VA

compensation for a service-connected disability, but you’re

receiving retirement or active-duty pay instead, or

-

The surviving spouse of a Veteran

who died in service or from a service-connected disability, or

who was totally disabled, and you're receiving Dependency and

Indemnity Compensation (DIC), or

-

A service member with a proposed

or memorandum rating, before the loan closing date, saying

you're eligible to get compensation because of a pre-discharge

claim, or

A service member on active duty who

before or on the loan closing date provides evidence of having

received the Purple Heart

You may be eligible for a refund of the VA funding fee if you're

later awarded VA compensation for a service-connected disability.

The effective date of your VA compensation must be retroactive to

before the date of your loan closing.

How much will I pay?

This depends on the amount of your loan and other factors.

Do you Qualify for a VA Funding Fee Exemption?

Borrowers are exempt from paying the

funding fee if they receive any disability payments from the VA or

are considered at least 10% disabled. Your VA mortgage lender

will work you to determine if you qualify.

Is the VA home loan program available to

Surviving Spouses?

YES. In order to get a VA home loan as the surviving

spouse of a Veteran, you’ll need a Certificate of Eligibility (COE)

to show your lender that you qualify for this benefit. Keep in mind

that you’ll also need to meet your lender’s credit and income

requirements to get a loan.

Additional VA Loan Programs

Interest Rate

Reduction Refinance Loan (IRRRL): also called

the Streamline Refinance Loan can help you obtain a lower interest rate

by refinancing your existing VA loan. For information specific to this

program, please visit the

VA website.

Native

American Direct Loan (NADL) Program: helps

eligible Native American Veterans finance the purchase, construction, or

improvement of homes on Federal Trust Land, or reduce the interest rate

on a VA loan. For information specific to this program, please visit the

VA website.

Adapted

Housing Grants: help Veterans with a

permanent and total service-connected disability purchase or build an

adapted home or to modify an existing home to account for their

disability. For information specific to this program, please visit the

VA website.

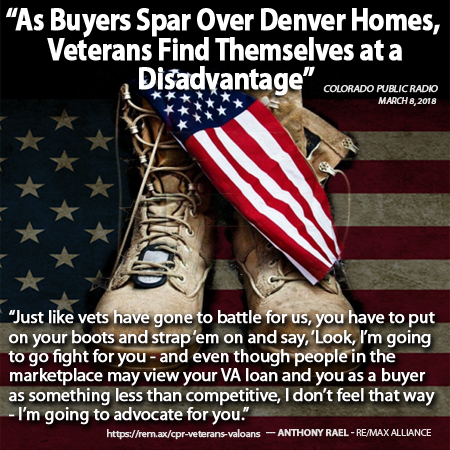

I created this image

after an interview I did with Colorado Public Radio in 2018. I was

discussing how Veterans can sometimes find themselves at a

competitive disadvantage in a seller's market. If you know anything

about the Denver housing market, it's been on a blistering pace

since 2014 with low inventory levels and extreme buyer demand fueled

by historic low interest rates. I simply cannot understand why some

listing agents and sellers don't consider a VA buyer with $0 money

down a viable option when bidding against cash buyers or financed

buyers with 10 or 20% down. While having a big down payment is

attractive, the goal is to get to closing and I have never had a VA

buyer not make it to the finish line in my 16 year career. There are

several factors to consider when writing a competitive offer in this

crazy market. As an honest and trustworthy REALTOR who values and

respects the dedication and sacrifice you have made to make our

lives better, I am prepared to go to battle for you. I look forward

to advocating on behalf of you and your family to secure a great

home! Call Ants at 303.520.3179 and let's chat.

I would like to personally thank ALL of our Service Members, Veterans and

eligible surviving spouses for your sacrifice to our country! I'm

always grateful for the opportunity to help military families buy & sell

homes in the Denver Metropolitan area. I work with retired military

buyers and sellers & assist military families who are relocating or transitioning from active-service to various civilian

employment with defense contractors such as Lockheed Martin, General

Dynamics, Northrop Grumman, Boeing & Raytheon. I consider it an

honor and a privilege to provide expert, professional real estate services

to military families and I look forward to help you buy or sell a home.

If you have any questions relating to

pre-qualifying for VA Home Mortgage and finding a great home in the Denver

metro area, call Anthony Rael at (303) 520-3179

Other VA Resources:

Are Veterans with VA Loans

at a competitive disadvantage?

VA Office in Denver, Colorado

VA Office in Denver, Colorado

United States

Department of Veterans Affairs

Federal Benefits for Veterans Booklet

[ RETURN TO BUYER'S

TOOLBOX ]

|

FIND YOUR DREAM HOME

NOW! |

SEARCH HOMES NOW!

HomesForSaleDenverColorado.com

MLS Listings Powered by remax.com |

SEARCH HOMES

NOW!

SearchHomesInDenver.com

Search ePowered by remax.com |

SEARCH HOMES

NOW!

HomesInColorado.info

ePowered by REMAX |

JUST LISTED

Just Listed : $200,000 - $2M

Just Listed : $200,000 - $2M

Just Listed : $100,000 - $500,000

Just Listed : $500,00 to $1M

Just Listed : $1M to $1.5M

Just Listed : $1.5 - $2M

Just Listed : $2M - $2.5M

Just Listed : $2.5M - $3M

Just Listed : $3M - $5M

Just Listed : $5M - $10M |

SEARCH HOMES IN DENVER

Search Homes : $300,000 - $3M

Search Homes : $100,000 - $500,000

Search Homes : $500,000 to $1M

Search Homes : $1M to $1.5M

Search Homes : $1.5 - $2M

Search Homes : $2M - $2.5M

Search Homes : $2.5M - $3M

Search Homes : $3M - $5M

Search Homes : $5M - $10M |

SEARCH CONDOS IN DENVER

Search Condos : $200,000 - $2M

Search Condos : $200,000 - $500,000

Search Condos : $500,00 to $1M

Search Condos : $1M to $1.5M

Search Condos : $1.5 - $2M

Search Condos : $2M - $10M |

|

New Homes In

Colorado | New Home Builders | Buying a New Home | 55+

Communities

First-Time Buyers | Luxury Homes | Energy-Efficient Homes

| New Construction

SearchNewHomesInColorado.com

Arvada, CO | Aurora,

CO | Boulder,

CO | Brighton,

CO | Broomfield,

CO | Castle

Rock, CO | Denver,

CO | Erie,

CO | Golden,

CO | Highlands

Ranch, CO

Lakewood, CO | Littleton,

CO | Parker,

CO | Thornton,

CO | Westminster,

CO | Wheat

Ridge, CO

/

RESIDENTIAL REAL ESTATE /

NEW HOME CONSTRUCTION /

RELOCATION /

FIRST-TIME BUYERS /

INVESTMENT PROPERTIES /

|

Buyer Guide |

Sellers

Guide |

New Home

Construction |

Buy a Home

Search for Homes |

Local Mortgage Lenders |

Mortgage Loans

metroDPA Down Payment Assistance

Program |

First-Time Buyers

Military/VA Home Loans |

Relocating to Colorado |

Active & Sold Listings

Sell a Home |

Property Values |

Denver Market Report

|

Refer a Client

realtor.com Reviews |

Meet Anthony

|

'JustCallAnts'

|

Connect with Anthony

© 2005-2026 ▪

ANTHONYRAEL.COM

| ALL RIGHTS

RESERVED | PRIVACY |

SITEMAP | HOME |

REFERRALS

Anthony Rael |

REMAX

Alliance - Denver |

3900 E. Mexico Ave, #970, Denver, CO 80210 | 303.520.3179

Each Office Independently Owned and Operated

|